Coffee With Catt: Issue #1 | Nevada Gold & Mining M&A

Nevada No 1 for miners, takeover predictions, PDAC notes, fund flows

This is the first in what I hope will become a regular bulletin on mining, metals and market themes we find interesting.

If you enjoy it, let me know and I’ll keep them coming.

PDAC: Critical Minerals Take Centre Stage

At the annual PDAC Mining Conference in Toronto this week, gold, silver and copper were front and centre as mining companies position themselves for what many expect will be a surge of investment tied to Trump’s critical minerals strategy.

The US military asked mining companies Friday 27th of February, a day before the Iran invasion for submissions in relation to 13 critical minerals used to make semi-conductors and weapons. More to follow on this in subsequent issues.

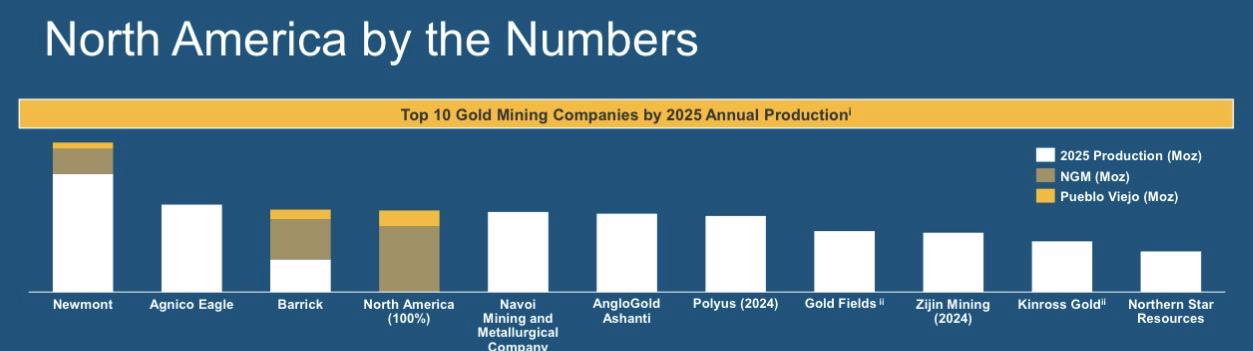

If gold and silver remain investors’ favourite metals in 2026 — as they were in 2025 — then Nevada, the #1 U.S. state for gold production and #3 for silver, is arguably the most important mining jurisdiction in the world.

Nevada mines should therefore command a premium valuation thanks to the rare combination of:

• world-class geology

• strong infrastructure

• stable permitting

• access to capital

Yet curiously Barrick Gold, the world’s third largest gold producer and owner of the most valuable gold assets in Nevada, trades at a significant discount to Agnico Eagle and roughly half the valuation multiple of Zijin Mining.

North America by the Numbers: The Gold Production Leaders

Barrick’s Nevada gold assets are the worlds most valuable

Yes, Barrick has geopolitically sensitive assets in the Congo, Mali and Pakistan. But to a buyer like Zijin — China’s dominant gold producer — those mines would likely be viewed as opportunities rather than risks.

Gold is gold.

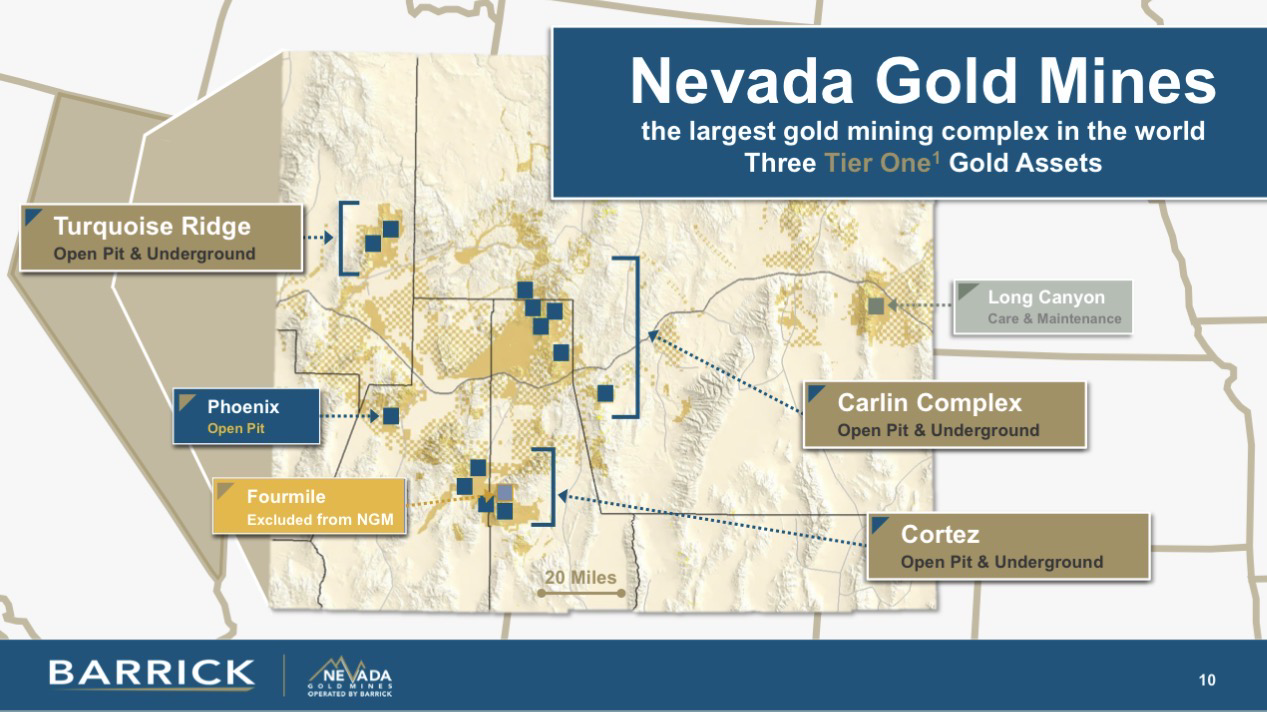

Nevada: The Golden Heart of Barrick

Most of Barrick’s Nevada gold mines are part of the Nevada Gold Mines joint venture with Newmont(61.5% Barrick / 38.5% Newmont).

The JV produced roughly 1.6 million ounces in 2025, compared with Barrick’s total production of 3.9 million ounces.

Add the nearby 'Fourmile ‘discovery of the century’owned 100% by Barrick — which could eventually produce ~750,000 ounces of gold per year — and Nevada could be half of Barrick’s future production and most of its value.

In other words:

A divestment by Barrick of its risky gold mines would unleash tens of billions of sharehareholder value by surfacing the value of its premium Nevada gold assets.

Nevada Gold Mines: The Core of U.S. Gold Production

Barrick and Newmont’s Nevada Gold Mines complex is the largest gold mining system in the world, combining multiple Tier-One assets that together form the strategic heart of U.S. gold production.

I have no inside information, but I believe Barrick will be broken up either by:

1️⃣ divesting its risky mines, or

2️⃣ being taken overone of its more richly valued peers.

Some context.

Back in October 2001, when I was working in the global mining group at Royal Bank of Canada, I made a call that Newmont would outbid AngloGold for Normandy Mining to create the world’s largest gold producer.

Newmont announced its winning bid a month later.

The logic then was simple:

The highest-rated companies have the strongest acquisition currency.

That logic applies to Barrick today.

One curious datapoint worth noting: Barrick did not attend the BMO Mining Conference this year, the most important gathering for major miners.

Interesting.

How to Play the Theme

Like Eric Sprott, we believe Hycroft Mining will continue to attract attention.

Hycroft controls the largest undeveloped silver-gold deposit in the United States, with an extraordinary 2.6 billion ounces of silver equivalent.

High-grade drilling results, stronger metal prices and potential M&A activity could all drive the share price. Watch this space.

I wrote about Hycroft earlier this year: www.cattcalls.com/commentary/hycroft-moonshot

The Return of the Comstock

Arlington is advising the rebirth of the legendary Comstock Lode through a new TSX IPO called Mackay Gold & Silver, expected to list in May 2026.

The discovery of gold and silver at Comstock in the 1860s helped finance the rise of San Francisco, the development of Nevada, and the early growth of what would become Wells Fargo Bank.

Historically the Comstock produced:

• 8 million ounces of gold (~35 g/t)

• 200 million ounces of silver (~700 g/t)

The company is named after John Mackay, the Irish immigrant who discovered the famous “Big Bonanza” in 1872 — one of the richest mining discoveries ever made.

CEO Darwin Green, previously behind HighGold and Onyx Gold, has assembled an unbelievable team.

I am personally a shareholder in Hycroft and Mackay, and will to add to my position in Mackay at the IPO.

Simon Catt and Peter Ruse from Arlington with Hycroft Vice President of Exploration Alex Davidson at the Core Shack at the PDAC Mining Conference last week. Alex is holding the core from recent drilling targeting high grade silver at the Hycroft mine.

Heard Down The Alley: Rumours from BMO: Coeur + Hecla?

One piece of PDAC conference gossip suggested that Coeur Mining CEO Mitch Krebs would very much like to see Coeur combine with Hecla Mining.

The strategic goal?

Entry into the S&P 500.

Both companies currently have market caps of roughly $17 billion.

A merger could create a combined entity larger than Pan American Silver, joining Newmont and Freeport as one of the largest mining companies in the United States.

Coeur’s flagship U.S. silver asset is the Rochester Mine in Nevada, which produced roughly:

• 6 million ounces of silver

• 60,000 ounces of gold in 2025

Given Coeur’s recent acquisition activity — including NewGold ($7B) and SilverCrest ($1.7B) — further consolidation would not be surprising.

Why M&A May Be About to Accelerate

Miners are beginning to see something important:

Generalist investors are finally paying attention.

As Keith Neumeyer, CEO of First Majestic, said during our recent Catt Calls SilverVerse webinar, pension funds are starting to return to the sector for the first time since 2011.

Watch the replay here:

Fund managers I speak to are also beginning to see meaningful capital flows into their mining funds.

Experience tells us this is the beginning of the next phase of this bull market.

Materials and Energy are today the top sectors for earnings upgrades in the S+P500.

The cavalry is about to join the battle.

The miners can see this happening in real time. That’s why more acquisitions are imminent; cashflows and inbound liquidity will drive valuations higher.

Gold Macro: The Setup

Two Federal Reserve governors, Kevin Warsh and Chris Waller, have recently suggested the risk to employment may be overstated and that falling inflation could give the Fed room to cut rates sooner than expected.

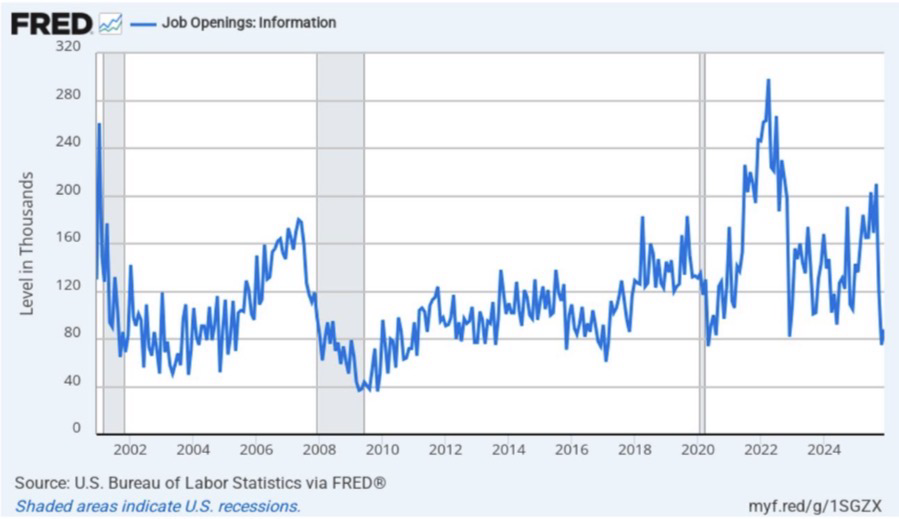

Labour Market Watch: Job Openings Cooling:

Job openings in the information sector have fallen sharply from post-pandemic highs — a signal that labour demand may be cooling faster than expected, potentially giving the Federal Reserve room to begin cutting rates.

The labour market chart above may be the one that matters most.

Despite the war in Iran Trump wants oil and inflation down to cut interest rates and boost the stock and bond market so American voters are happy ahead of November mid term elections.

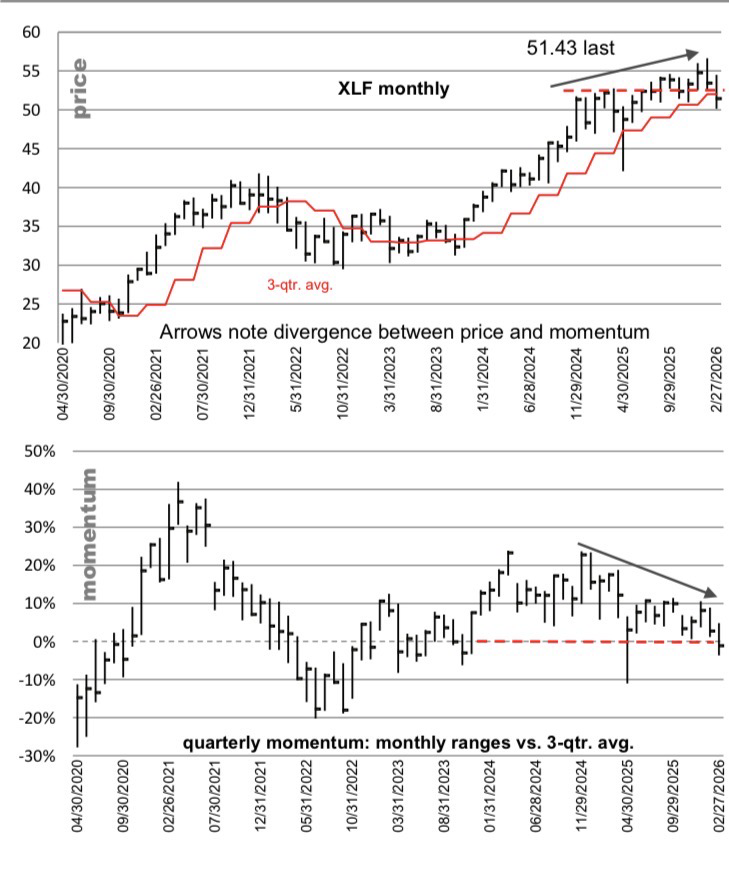

Chart of the Week: Financials Showing Momentum Divergence:

Price in the financial sector ETF (XLF) has continued higher while momentum has weakened — a classic divergence that often precedes policy easing as central banks move to stabilise financial conditions. Thanks to Michael Oliver of MSA.

Nvidia’s recent share price weakness despite ‘perfect’ results is further evidence that the Mag-7 leadership is tiring.

More importantly, Michael Oliver at Momentum Structural Analysis notes that the Financial Sector ETF (XLF) is beginning to roll over.

The American economy is weakening, Trump’s Fed will likely respond with rate cuts to support employment and markets.

Act 2 is about to start

The end of hostilities in the Middle East could be the starting gun for the next stage of the precious metal led commodity bull market.

Mining companies and mining funds are seeing Big Money interest for the first time since 2011. The miners cashflow multiple are undemanding. The big producers will be the first M+A targets. Get your popcorn, charge your glass, the Second Act is about to start.

Simon Catt

Director, Arlington Group Asset Management

Host, Catt Calls