Coffee With Catt - Issue #7: Casino Mentality

One More Roll of the Dice

The stock market is a casino, but you want one more winning roll, then you’ll quit because you’re up big. The croupier smiles as he sees you beckon him to deal you back in…

Are you feeling lucky?

“There is no training, classroom or otherwise, that can prepare for trading the last third of a move, whether it’s the end of a bull market or the end of a bear market.” — Paul Tudor Jones

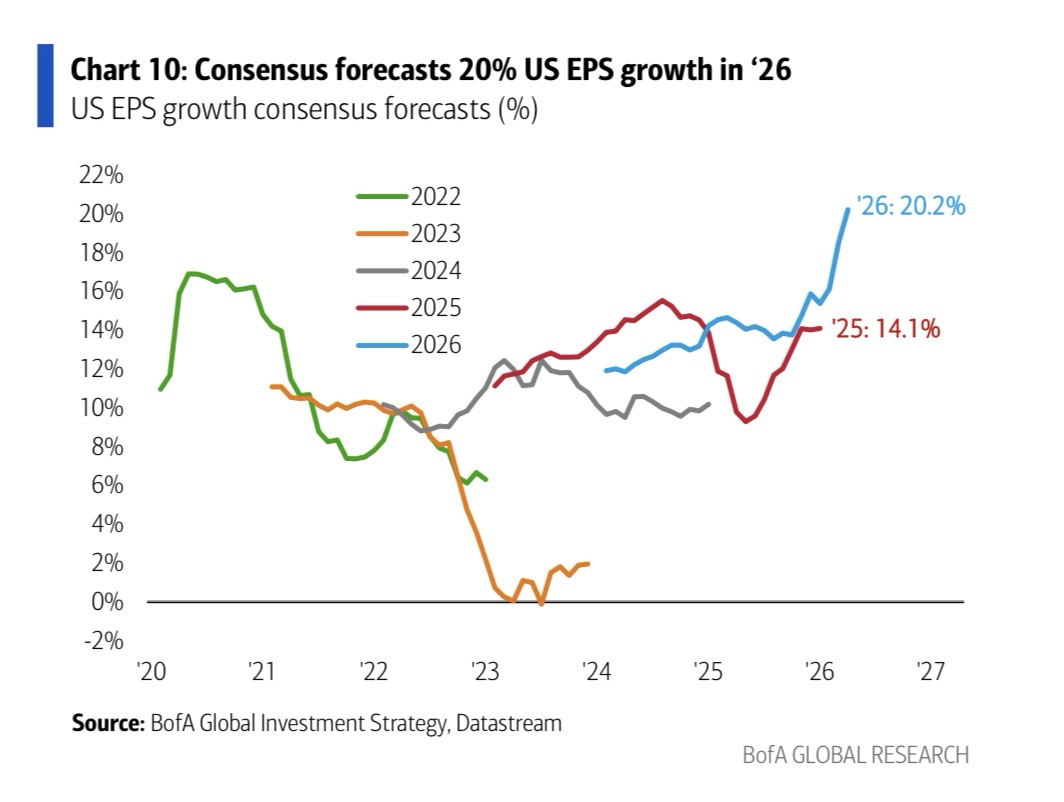

Two things matter most to the stock market — earnings and the interest rate at which we discount those earnings.

Earnings growth in 2026 is the best in over a decade.

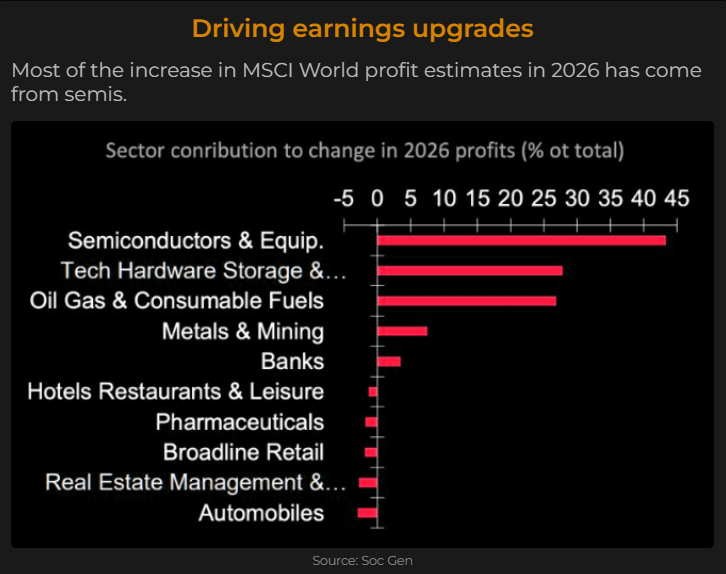

Technology and natural resource company earnings have led the S&P 500 higher:

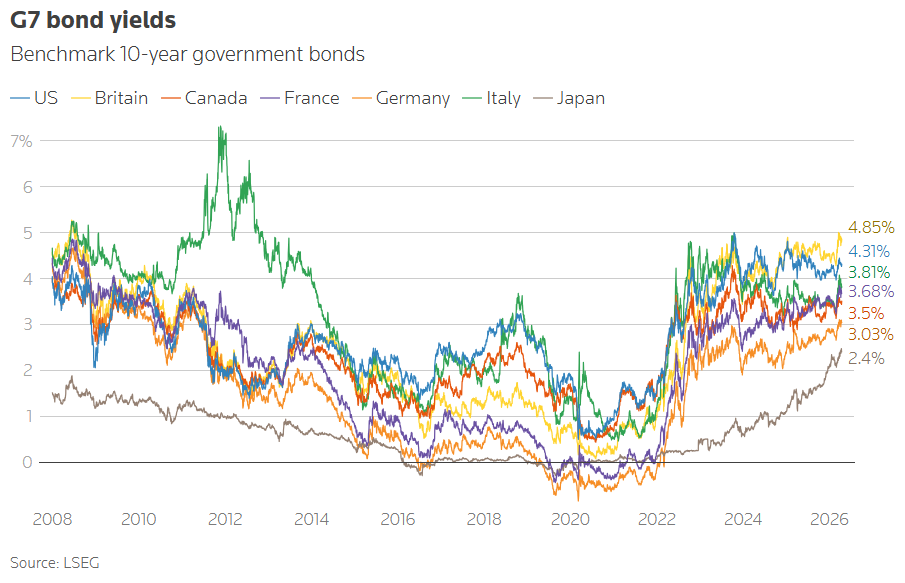

However, borrowing costs are also higher.

Higher energy prices flowing from the war in Iran have added upward pressure on G7 sovereign debt yields:

The benchmark yields for the United Kingdom and Japan — both net energy importers with sizeable deficits and debt burdens — have increased the most.

The cost of borrowing for the UK government, measured by its 30-year ‘Gilt’ yield, has risen sharply.

The bull case is that ‘peace’ in Iran should allow bond yields to moderate and risk appetite to rally.

The Stock Market Believes Peace Is Coming To Iran

While Trump’s foreign adventurism is restrained by the American voter, the Iranian government is bankrupt without oil production. UK fund manager and commentator Hugh Hendry explained recently:

“Iran’s oil system is not built to pause. It’s built to flow.

It has to move. Iran and its system have to move continuously from the rock underground to the tanker in the harbour to the Chinese buyer in Asia.

Pause long enough, and the whole machine breaks.

…with a ‘total export blackout’ having effectively started this past weekend, Iran now has about 15 days before it has to begin production shut-ins, which then have to be fully completed by day 30, or sometime around May 20.

And global capital markets have already moved to price that eventuality in.”

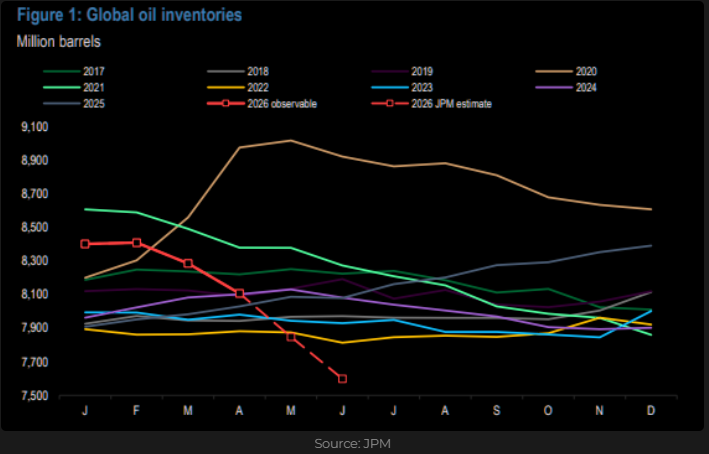

However, what if the Iranian blockade drags on and destroys some of Iran’s productive capability? That could drain inventories fast. Here is JP Morgan’s prediction:

Is this the real aim of Trump’s blockade? To break Iran’s economy and facilitate regime change? This would spell trouble for energy importers like the UK and Japan.

If Iran is still awash with trapped oil by the end of May, then disappearing global inventories become the trade.

Petroyuan Replacing Petrodollar?

The grand bargain known as the ‘Petrodollar’, which has been an important source of demand for US Treasury bonds for thirty years, is unravelling.

In 1974, then-US Secretary of State Henry Kissinger negotiated with Saudi Arabia that they would buy oil in US dollars and recycle the proceeds into US assets. In return, the US offered Saudi security guarantees. Times change.

China is now a more important customer for Middle Eastern and Russian oil and gas producers than the United States and prefers to pay in its own currency, the Renminbi, which is convertible into gold.

Although it is logical that the US invasion of Iran marks a retreat from the grand bargain known as the ‘Petrodollar’, it matters less than you think.

The Yuan Carry Trade?

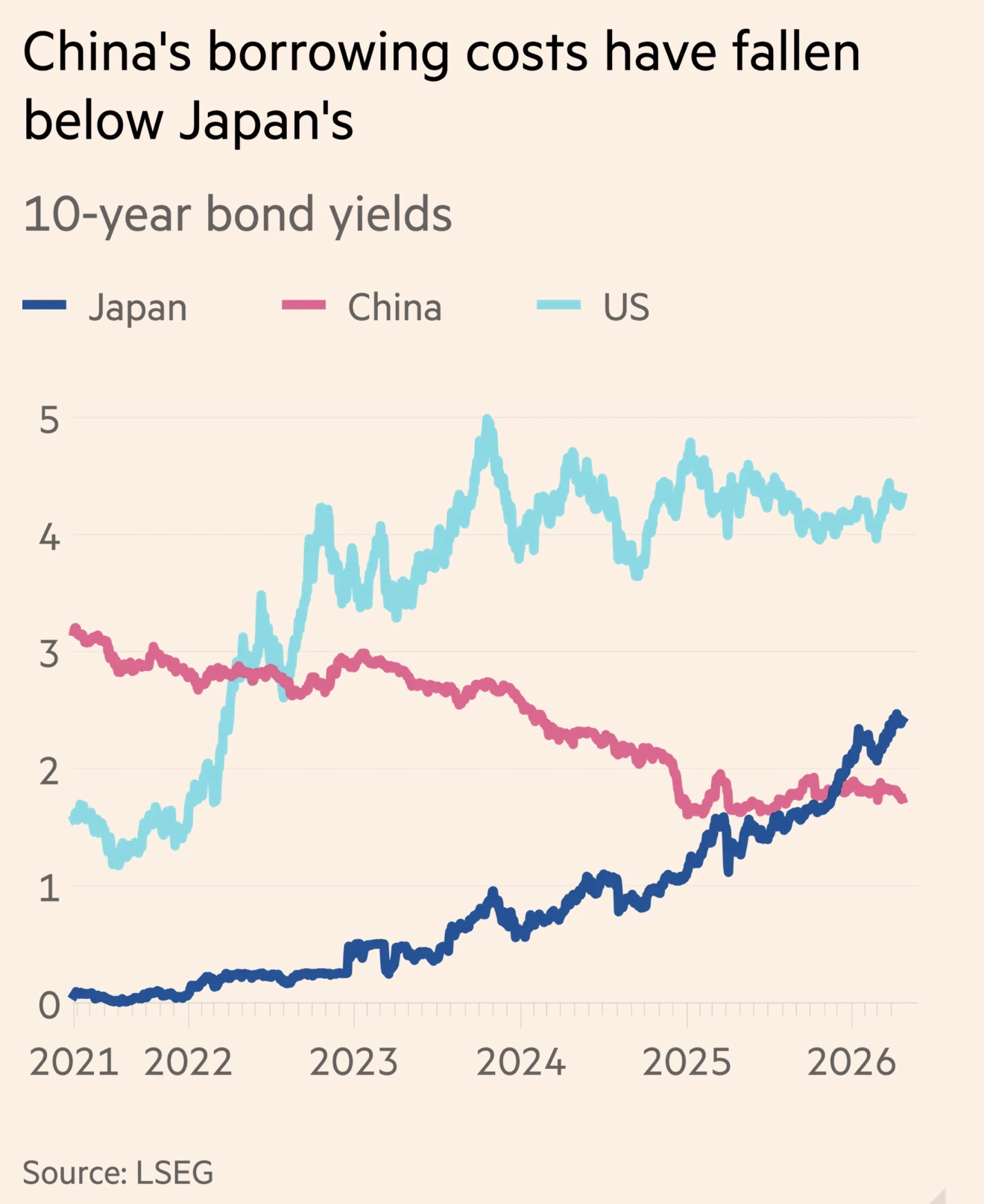

China has replaced Japan as the lowest-cost sovereign borrower of any major country as it fights deflation at home.

China’s benchmark 10-year bond interest rate has fallen from over 3% to less than 2%.

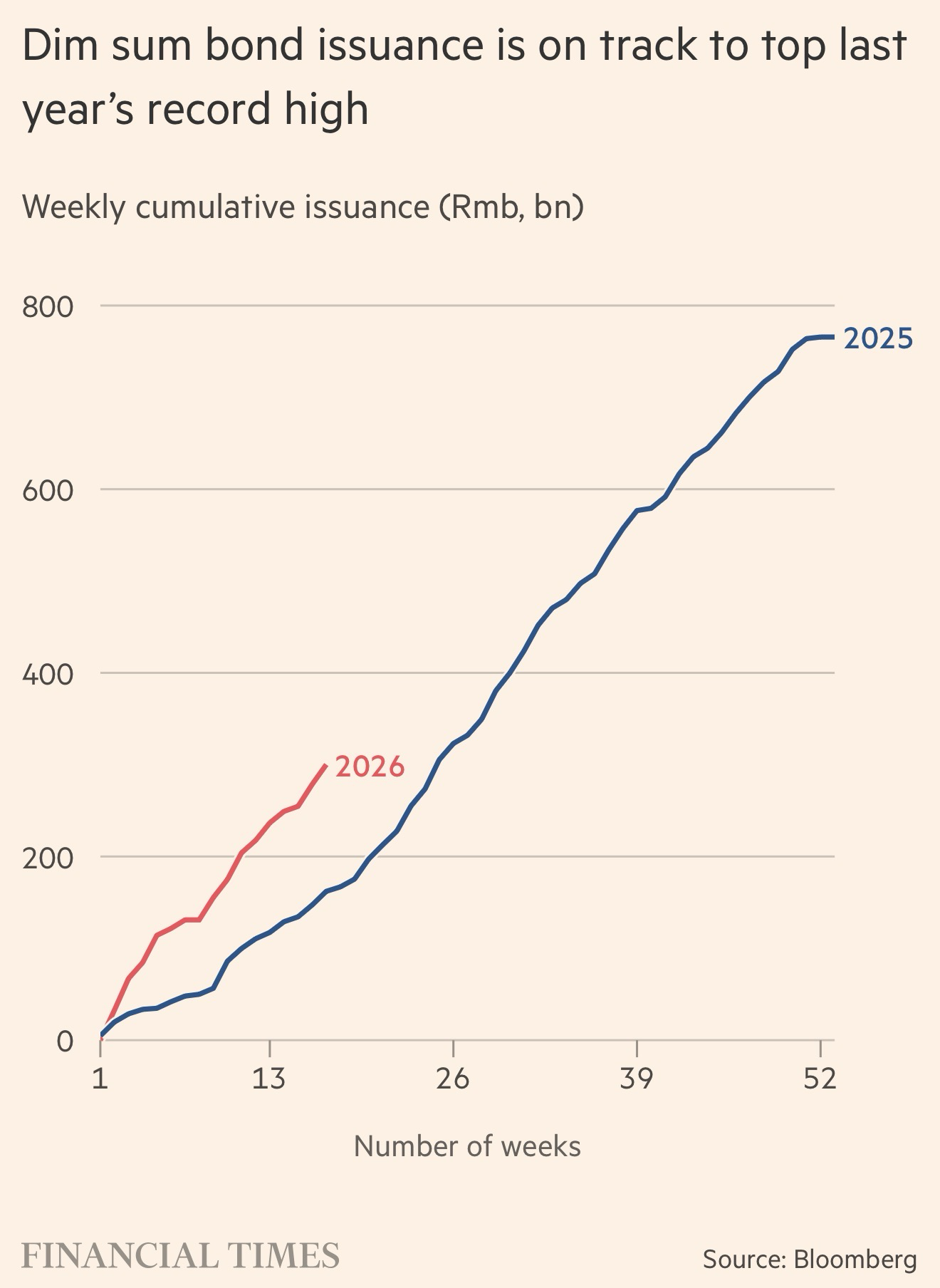

Foreign governments are increasingly accessing lower Chinese interest rates by issuing ‘Panda bonds’ inside China and ‘Dim Sum’ bonds outside China.

Total 2026 Dim Sum bond issuance of about RMB 300 billion, or US$44 billion, is modest compared to the US Treasury market, but the fact that foreign RMB issuance doubled in a year seems important.

Portugal became the first European country to borrow in Yuan in April when it issued a €249 million 8-year bond at 1.765%.

However, total foreign ownership of Chinese bonds is modest at about $1 trillion out of total issuance of $25 trillion.

Yenmageddon

Japanese deflation has ended after thirty years and yields have rallied from zero to almost 3%.

This matters because, for thirty years, Japanese savers have been exporting their savings into risk assets globally — especially to its ally, the United States.

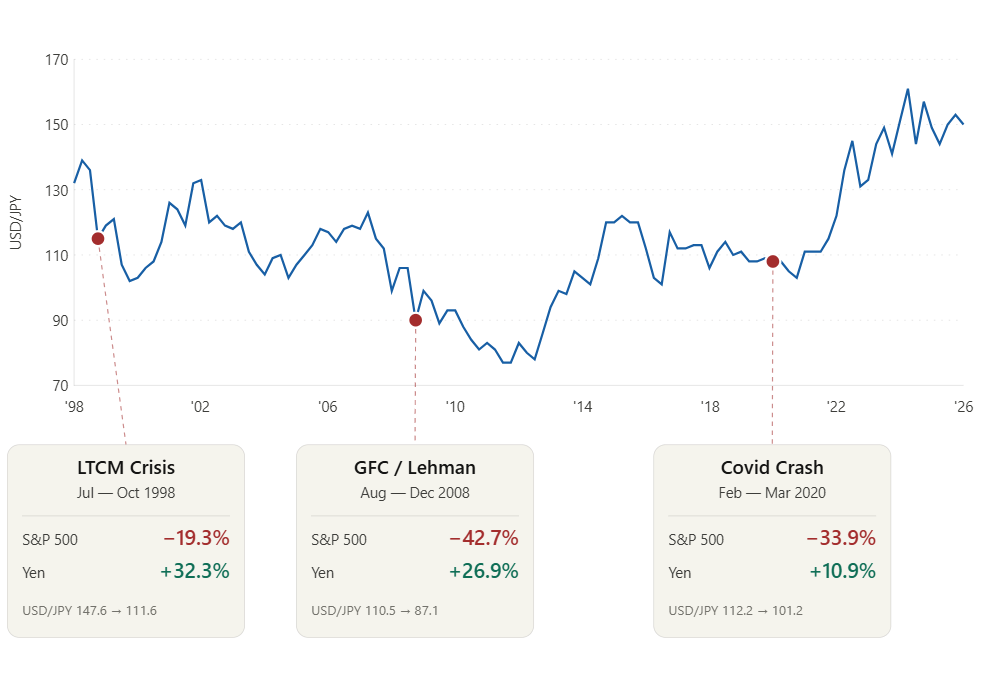

The risk is that rising Japanese inflation and interest rates suck those savings back home to Japan. The ‘repatriation trade’ is also known as the unwind of the Yen Carry Trade.

The historical cause of the collapse of the Yen Carry Trade is always the same:

Cheap yen funding leads to crowded global risk assets and complacency about volatility.

A dovish US Fed pivot, a hawkish Bank of Japan pivot, or a shock like Covid.

Yenmageddon could mean a ~30% retracement in the S&P 500.

Dry Tinder

On June 16th and 17th, both the Fed and the BOJ meet to consider interest rate policy. The risk is that the Fed pivots dovish while the Bank of Japan raises interest rates to cool inflation. Stock market valuations are at all-time highs.

Currency Chaos

Trump and Bessent want a weaker dollar, while Japan’s Ministry of Finance wants a stronger yen.

The tinder is dry and all we need is a spark.

Maybe June’s monetary policy meetings are the match that starts the fire.

Catt Call

When everything goes parabolic like today, it is usually the end of the cycle. But the party inside the casino is so good you can’t leave.

Stay as long as you dare.

But don’t forget to book your taxi home

Disclaimer

The content on this website is provided for information and commentary purposes only. It is not intended to constitute, and should not be construed as, investment advice, a personal recommendation, or a financial promotion within the meaning of applicable financial services legislation. The views expressed are solely my own and are provided in my personal capacity. They do not represent the views of Arlington Group Asset Management Limited or any affiliated entity. No reliance should be placed on the content for the purpose of making investment decisions.

Risk Warning

Readers are responsible for conducting their own due diligence and for obtaining independent professional advice before making any investment decisions.

Investing in financial markets, particularly in small-cap and junior resource companies, involves risk, including the possible loss of capital. Past performance is not a reliable indicator of future results.