Coffee With Catt: Issue #3 |Investing For Wartime

Gold, guns and war minerals

Two outcomes of the war in Iran seem certain:

A Sovereign Debt Crisis

A decade of military rearmament

There are three ways investors can position themselves:

Gold and silver in preference to fiat currency

Critical minerals essential for military uses

Energy and energy minerals

War and higher oil prices anticipate a sovereign debt crisis in two ways;

Higher bond issuance to pay for the war and,

Higher oil prices force oil importing nations like Japan, UK and China to sell their inventory of foreign assets to finance the higher cost of buying energy.

Add forced selling of US shares and bonds to deteriorating US presidential credibility and you have the ingredients for a sharply lower US dollar.

The corresponding move higher in commodities which are priced in dollars could take your breath away.

In previous weeks we discussed some favourite gold and silver miners:

Next week we will talk about some fabulous dividend-paying coal miners. Diminishing exports of Middle Eastern oil and gas means more switching to coal for electricity — and higher coal prices.

This week I am going to highlight my favourite investment that captures the critical minerals for war theme.

This company’s billion-tonne resource in Victoria, Australia combines established infrastructure with a globally significant endowment of four of the top five US critical minerals, as identified by the 2025 USGS

Australia is building its first guided missile factory with first production in 2027.

Gippsland Critical Minerals (GCM) Fingerboards Project will produce important amounts of four increasingly valuable rare earths whose supply is controlled by China and that the West needs now for magnets, missiles and semi-conductors. Read on for details.

Some conversations we had with investors thisweek:

“I’ve got a new tungsten play”

“I wish I had more cash!”

“Iran will decide when this war ends”.

War impact down-under:

West Australian iron ore and gold producers are scrambling to secure supplies of diesel fuel in Asia while some freight rates to China have doubled.

Aussie fertiliser distributors report China has torn up their supply contracts as it hoards fertiliser for its own farmers.

Qantas charged me the same airfare all over again to avoid a Dubai stopover on my Perth to London journey next week.

A Shakka Of Investors And Quokkas

This week I met with some mining fund manager buddies passing through Perth after the 2026 annual Euroz Hartley’s annual Rottnest Conference where a shakka of investors attended ‘Rotto’ the sun-drenched-wind-blown island 20km off the coast of Perth known for its indigenous Quokka’s.

A group of quokkas is called a “shakka”.

Every year trusting tourists come looking for quokkas and mining investments

English and Canadian visitors were impressed with the scale and established infrastructure of the West Australian Gold Fields; “much bigger than Canada” commented a sunburnt Canadian fund manager.

Amen brother.

The stock pickers noted that the larger Aussie gold miners had significant low grade stockpiles available for processing through their domestic gas fired power plants if the diesel fuel powering their trucking fleet has to be rationed.

Gold and Guns

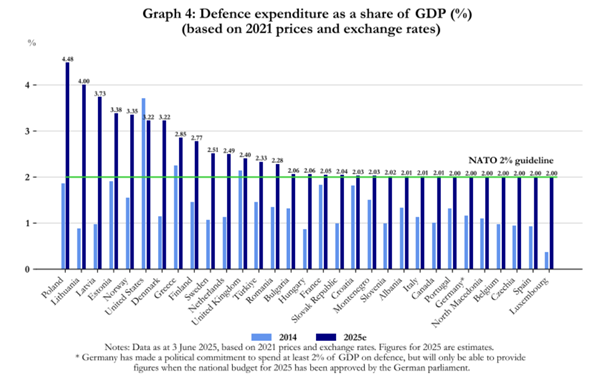

Poland, the largest military spender in the NATO alliance after the United States plans to spend US$50 billion or almost 5% of its GDP in 2026 on defense. In its most important rearmament since the Cold War Poland said it wants to build the largest land army in Europe in response to Russia’s invasion of Ukraine in 2022.

Poland said this month it would potentially sell (has sold?) or revalue US$13 billion of its US $80 billion or 550 tonne gold reserve to fund defence expenditure.

Poland bought 100 tonnes of gold in 2025 and plans to increase its holding to over 700 tonnes.

In times of war, gold is more useful than dollars.

Poland spends the most in the NATO Alliance on defence as a percentage of its GDP

A Perfect Project For Magnets and Missiles

Nine years ago in 2017 I visited the Fingerboards Project today owned by Gippsland Critical Minerals (GCM). This is a project whose time has come with the recent award of Major Project Status by the Australian Federal Government.

This week we caught up with Gippsland Critical Minerals CEO Michelle Wood on why this project has become ‘critical’ for Victorian jobs and Australian mineral exports to our allies.

“Rare earth magnets are in everything we use for modern applications, from our cell phones to defence applications from F-35s and Tomahawk missiles and beyond.”

Kevin Colborne, JP Morgan

Mines of War

On February 27th 2026 - the day before the US and Israel invaded Iran - the United States Department of War issued a new Request for Project Proposals (RPP) focussed on strategic and critical minerals.

The Department of War (DoW) has prioritised identification of supply chain alternatives for defence-critical minerals used in the production of aircraft, missiles, semiconductors, and other defence technologies.

The following minerals were requested by the DoW:

arsenic

bismuth

gadolinium

germanium

graphite

hafnium

nickel

samarium

tungsten

vanadium

ytterbium

yttrium

zirconium

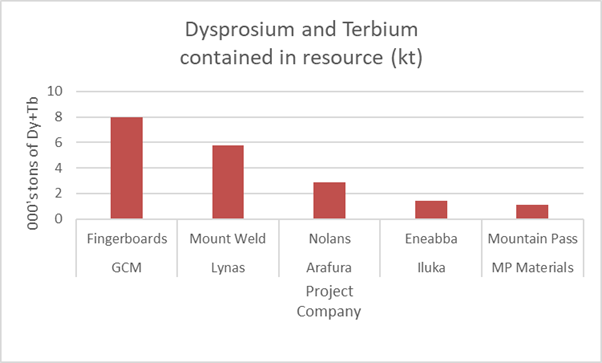

Gippsland Critical Minerals (GCM) contains hafnium, samarium, ytterbium, yttrium and zirconium plus other important critical minerals like dysprosium and terbium.

Western Supply Chains Cost More

The US and Japanese government have both given minimum price floors of US$110/kg for ‘magnet metals’ neodymium (Nd) and praseodymium (Pr) oxide to rare earth producers MP Materials in the United States and Lynas Rare Earths in Australia.

Nd and Pr prices were around US $60 per/kilo a year ago.

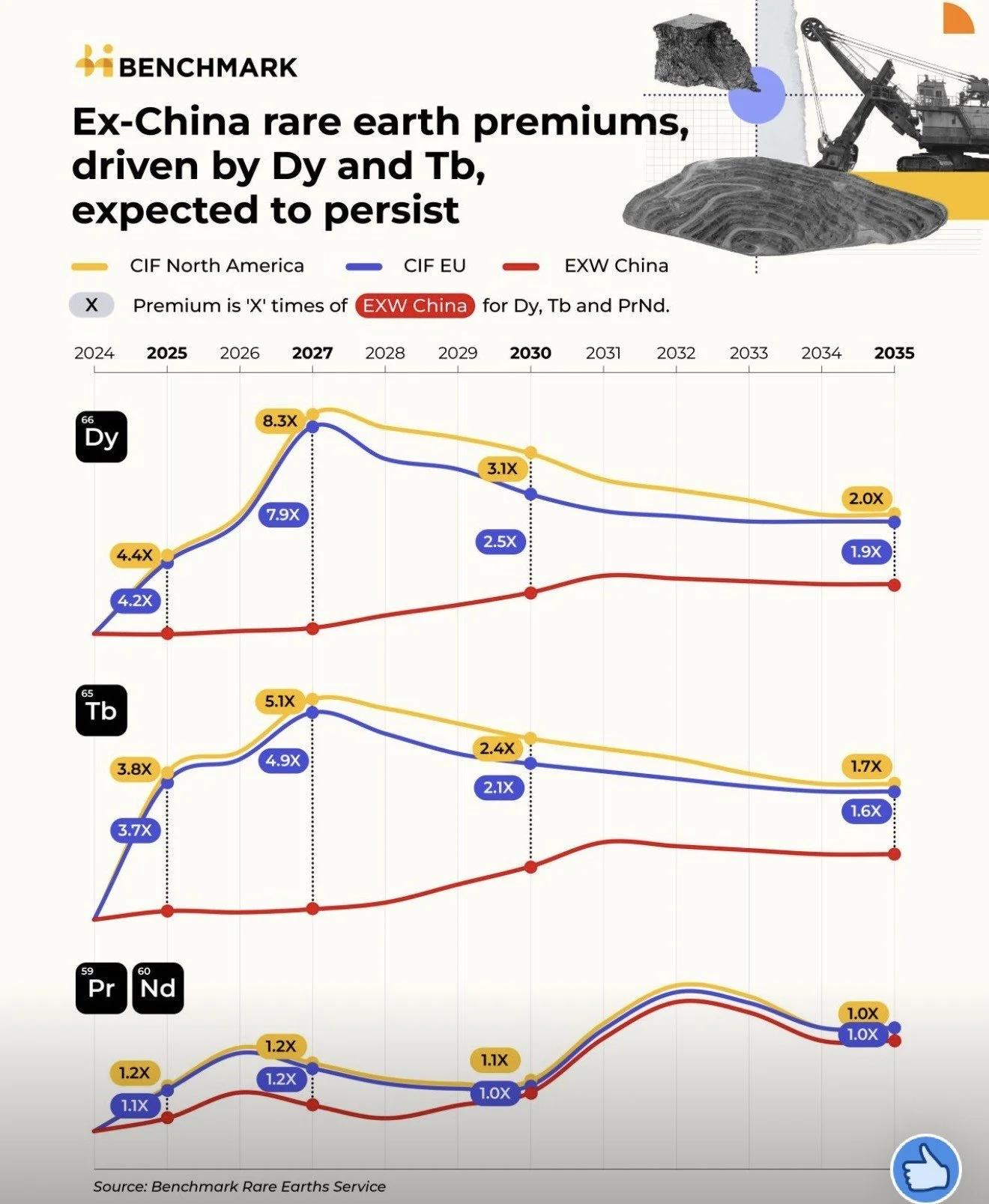

Heavy rare earths, dysprosium (Dy) and terbium (Tb), used for high temperature aerospace magnets are even more valuable than Nd Pr with prices of over US$200/kg for Dy and $4000/kg ex China.

Ex China rare earth prices are forecast to increase to 5-8 times Chinese prices by Benchmark Mineral Intelligence. Terbium oxide trades at ~US$4500 in the US and Europe, up over 100% year to date versus only $900 per ton in China.

The premium for ex Chinese supply of Dysprosium and Terbium is forecast by Benchmark to be 5X to 8X Chinese prices.

Magnets And Missiles

Fingerboards was discovered by Rio Tinto in 2004, before rare earths were valuable as the source materials for the world’s most powerful magnets.

The heavy rare earths weaponised by China are concentrated in the Fingerboards Project, which should produce ~7% of the world’s terbium, dysprosium and zircon when in production in 2030.

Fingerboards was recently awarded “Major Project Status” by the Federal Government of Australia, alongside a Victorian Government that has reformed its approach to mining, issuing six new mine permits in the September 2025 quarter alone.

In addition to Zircon (Zr), Dysprosium (Dy) and Terbium (Tb) Fingerboards rare earth project is also an important future source of Lutetium (Lu) for high precision medical imaging, Yttrium (Y) for lasers and Samarium (Sm) for high temperature magnets.

Check out the MP Materials website for some useful background on these critical minerals: https://mpmaterials.com/materials/

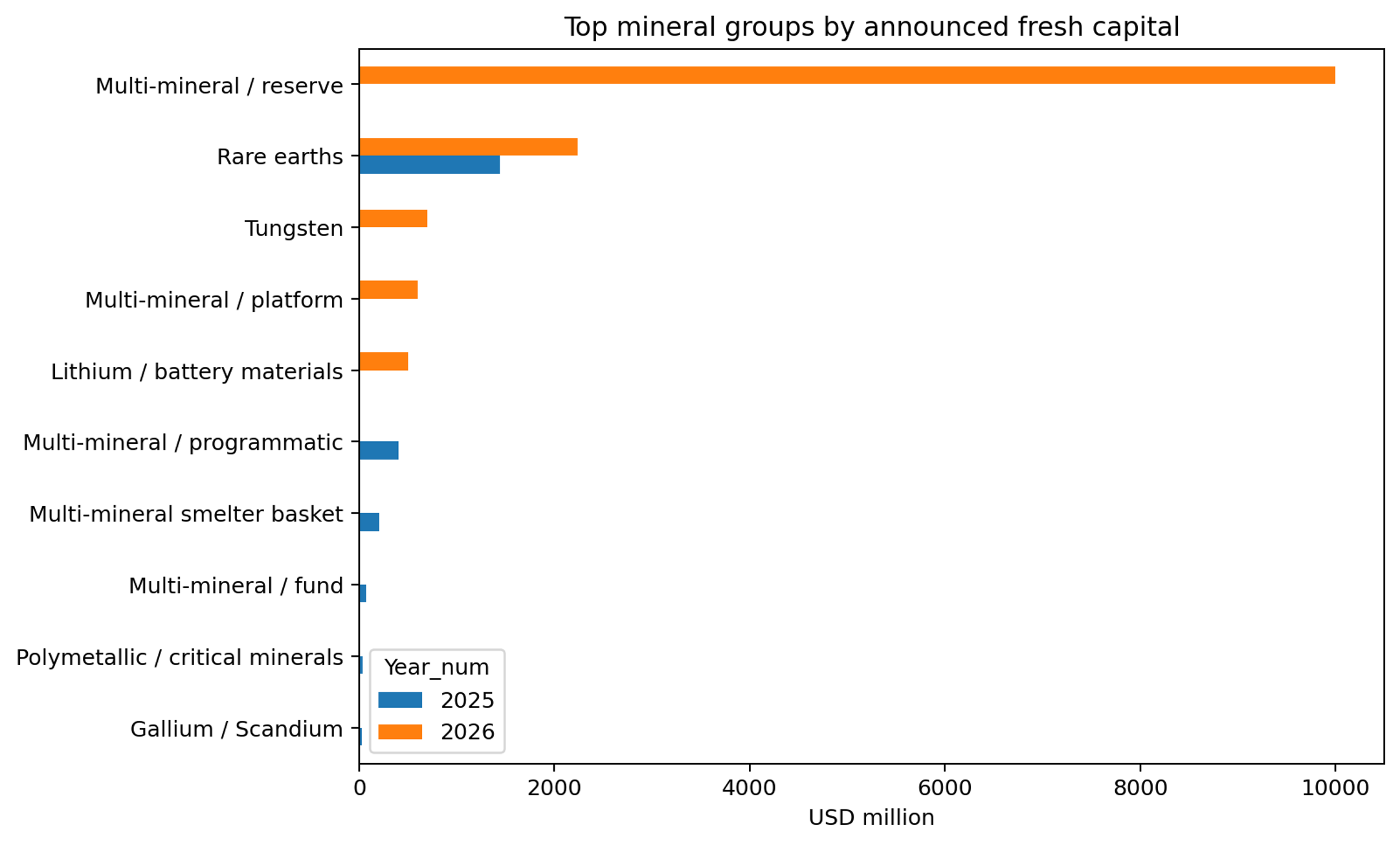

The focus of US critical mineral funding under the Trump administration has shifted from battery metals to rare earths and accelerated in 2026.

The Numbers That Matter

I first invested in the Fingerboards Project in 2017 and am now tripling my bet in this billion tonne asset because, for the first time ever Australian politics, international capital and local social licence are aligned.

Gippsland Critical Minerals (GCM) the owner of 100% of the Fingerboards Project has a Net Present Value of well over A$1 billion versus a current private valuation of A$75 million.

GCM is owned 80% by private company REZir and 20% by Appian Capital.

(Let me know if you are interested to know more about investing in GCM. Even my mum is investing in this valuable project with a unique endowment of critical minerals.)

Catt Call 🐾

No one knows how or when the Iran war ends.

But the direction of travel is obvious.

More defence spending.

More competition for scarce resources.

More pressure on supply chains.

And somewhere - heard down the alley before it hits the headlines - capital is already moving.