Coffee With Catt: Issue #4 | War, Drones & Dividends

Back To London

This Easter the Catt family travelled back to the birthplace of my four children — London.

Central London was busy. We drove past an Easter play being performed in Trafalgar Square as Nelson looked down from atop his column. The kids saw Matilda, and Amore Mio and I saw SIX for date night.

“As Samuel Johnson said, “He who is tired of London is tired of life.”

My six-year-old and I enjoyed watching the moving map on our Qantas flight from Perth via Singapore across the Black Sea. We chose to avoid Dubai and Doha this time. Changi Airport in Singapore was wonderfully dull.

War On My Mind

The air traffic heading to London from Asia since the war in Iran now passes through a narrow corridor in Azerbaijan’s airspace.

Russia’s warm water port of Sevastopol, home of the Black Sea Fleet since 1783, appeared on the screen in the darkened Qantas cabin. Then we flew past Ukraine’s staunchly defended main maritime gateway — the port of Odesa.

We watched Warsaw slide past, where Europe’s largest land army is being assembled, and then on to Berlin — once divided into Russian, French, American and British quarters in the aftermath of WWII.

War on my mind.

Reading the open letter below, sent this week from Oleksandr Yakovenko, founder of TAF Industries — one of Ukraine’s largest drone makers — explains succinctly how the concept of “warfare”, and our sovereign nations’ ability to protect our “peaceful” lives, has changed completely since Russia invaded Ukraine in 2022.

Industrial Darwinism

“Dear Mr. Armin Papperger, CEO of Rheinmetall,

When you called Ukrainian drone manufacturers ‘Ukrainian housewives with 3D printers in their kitchens’, you demonstrated how deeply the European defence establishment still fails to understand the nature of modern warfare.

This is not about emotions. This is about battlefield reality.

Here are the figures your industry refuses to acknowledge:

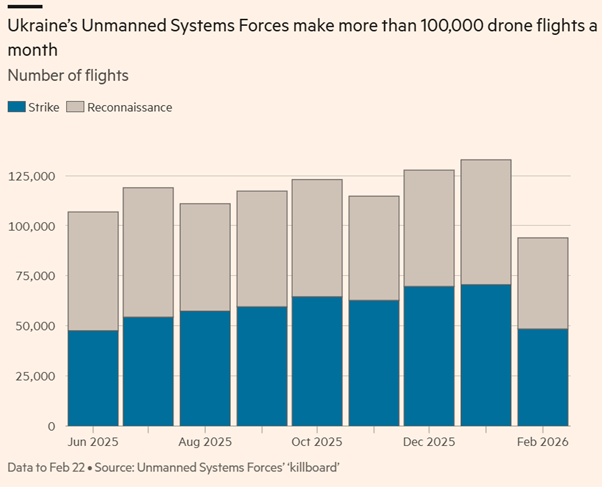

In 2025 alone, Ukrainian drones carried out 819,737 confirmed strikes.

They accounted for 90% of all combat losses of the Russian army — more than all other types of weapons combined.

A single company, TAF Industries, produces up to 100,000 FPV drones per month. Over any given 90-day period, the products of my company alone have more confirmed hits than your entire fleet of equipment over its entire history of combat use across all conflicts. And most importantly — I built this company and achieved these results in two years, not fifty. Think about that.

Our drones achieve greater kinetic effect in three months than your flagship platforms have in half a century.

Why? Because the battlefield has changed, while your business model has not.

Russian electronic warfare has rendered GPS-guided Western munitions (Excalibur, GMLRS, etc.) almost ineffective.

Expensive and complex systems designed for wars with air superiority and conventional “peer-on-peer” conflict have become easy targets for drones costing $500–2,000 that attack them from above.

The cost-effectiveness ratio has been turned upside down: one 120mm Rheinmetall shell or one anti-tank missile costs more than a dozen of our drones — yet our drones still prevail.

This is not a ‘Lego game’.

This is industrial Darwinism in real time.

We iterate weekly. We lose factories to missile strikes and rebuild them within weeks. We print parts in basements and deploy 100,000 strike systems per month, while your engineers still require 3–5 years and hundreds of millions of euros to certify even minor upgrades.

The war in Ukraine is not a temporary anomaly. It is the first true drone-industrial war

And it has already proven that outdated European platforms - no matter how expensive or ‘serious’ - are becoming increasingly irrelevant if they do not integrate the very technologies you are mocking.

So when you say “this is not innovation”, I hear something else:

“We do not want to admit that the future is being written in Ukrainian workshops, not in Düsseldorf offices.”

The hashtag #MadeByHousewives is trending for a reason. Because these ‘housewives’ destroy more enemy equipment every month than entire European armies do over full campaigns - and they do so while your industry continues to sell 20th-century solutions at 21st-century prices.

The invitation stands, Mr. Papperger. Stop laughing at the kitchen table.

Come and learn how the war of tomorrow is actually fought.

Because the next time someone asks, “Who needs tanks in the age of drones?”, the answer may be simpler than you think:

Those who still believe in 1979 will lose to those who are building in 2026.

With respect (but with facts),

Oleksandr Yakovenko

Founder of TAF Industries

One of those ‘Ukrainian housewives’

Dividends of War

Coal was the energy source that powered the Industrial Revolution, which began in Britain around 1750 before spreading to Continental Europe and then the United States by around 1840.

Britain’s coal production grew from 5 million tons in 1850 to over 60 million tons by 1900, fuelling new machines such as the steam engine.

Although renewables overtook coal in the first half of 2025 as the dominant form of electricity production thanks mainly to the growth of solar generation in China, coal in Asia is enjoying renewed popularity in 2026 in the face of exploding Qatari gas production.

Australia’s Newcastle Coal benchmark is up ~ 30% in 2026 to $140/ton compared to a ~ 300% increase in steaming coal prices to over $400/ton in 2022 following the Russian invasion of Ukraine.

As the Economist pointed out this week, most of the missing Qatari Liquified Natural Gas (LNG) was bound for Asia so this is where coal and LNG prices look well bid for the medium term.

“This time the energy crisis hit hardest in Asia, where many large energy importers, in particular China and India, still dig up and burn lots of coal. Their mines’ output can be increased to offset the LNG shortfall in a matter of months.”

“As the energy crisis drags on, however, the coal market is likely to get hotter. Japan, South Korea and Taiwan, all big importers of both LNG and coal, find themselves in a similar predicament to Europe four years ago.” (The Economist)

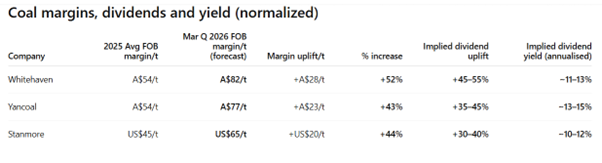

The three largest Aussie coal producers are: Yancoal, Whitehaven and Stanmore.

Yancoal Australia offers the clearest proposition for investors focused on income. The business generates strong, consistent cash flow from its thermal coal portfolio and applies a high payout ratio, which supports reliable dividends. Pricing can lag spot markets, but over a full cycle Yancoal typically delivers the highest and most stable yield in the sector.

Whitehaven Coal presents a different angle: less about current yield, more about upside in dividend growth. Its mix of thermal and metallurgical coal creates stronger operating leverage when prices rise, which can drive sharp increases in free cash flow. As a result, dividends tend to move in steps, making Whitehaven the name most likely to surprise on the upside in a strong pricing environment.

Stanmore Resources is the more cyclical option, with returns tied to metallurgical coal markets and steel demand. Dividends are less predictable and the base yield is typically lower, but when met coal prices strengthen the company can generate rapid cash flow expansion. This makes Stanmore a higher-risk, higher-upside yield play, suited to investors willing to accept more volatility for potential gains.

Drill Baby Drill

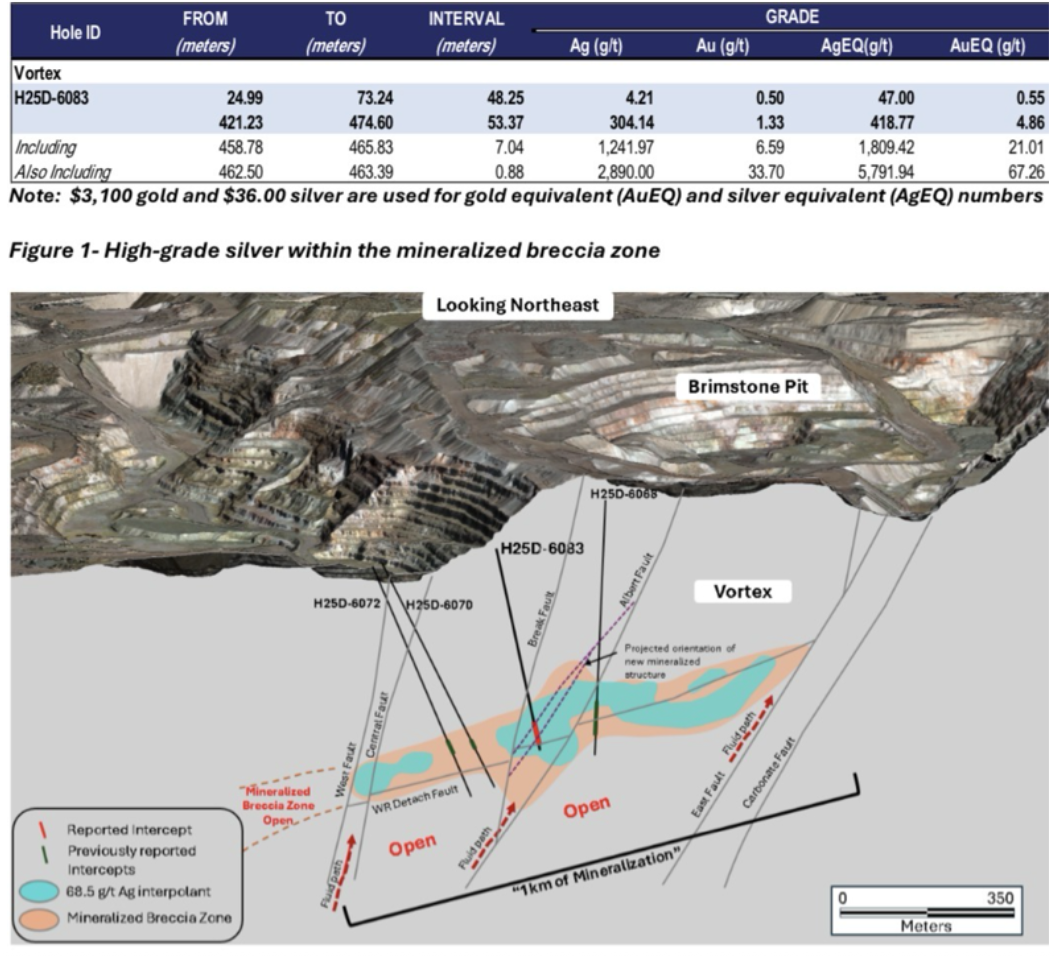

Hycroft Mining (HYMC:US) released what may be the most important exploration results for over a year from America’s largest undeveloped gold and silver project in NevaDA which produces ~ 70% of America’s gold..

Hycroft announced hole H25D-6083:

7 metres at 6.59 g/t gold and 1,242 g/t silver (~21 g/t gold equivalent) in the emerging “Vortex” discovery.

This is the first time Hycroft has added high-grade gold alongside silver in either of its Vortex or Brimstone discoveries.

Gold mines grading greater than 5-10gpt gold are very rare and create fabulous wealth.

Most gold mines are less than 1gpt.

Hycroft’s neighbouring Ken Snyder (now Midas) gold mine, along with the Goldstrike royalty, helped create the foundational wealth of Franco-Nevada (FNV:TSX, C$69 billion market capitalisation), the best-performing Canadian mining company since its inception in 1982.

Franco Nevada’s Ken Snyder mine in 1998 had a mineable reserve of 2.726 million tons at 1.115 oz (35 grams) per tonand 12.82 oz (399 grams) silver per ton containing ~3.04 million ounces of gold and ~35 million ounces of silver.

At year end 1998 gold and silver prices of US$289/oz and $5.40 the Ken Snyder mine’s value per ton of ore was about US$400 or in 2026 dollars about US$800/ton.

Using the current gold $4600/oz and silver $73/oz prices Hycroft’s latest Vortex Hole H25D-6083 drilled 7 metres at 6.59gpt gold and 1242 silver is worth about US$3800/ton.

In 2026 dollars, Hycroft’s latest drill hole is about five times more valuable per ton than Franco’s Ken Snyder Mine, one of the highest grade gold and silver mines in the history of America.

Hycroft are doubling the number of drill rigs exploring at its Vortex and Brimstone discoveries in the coming months. This is good news for Hycroft shareholders - accelerating the pace of discovery just as the head of exploration Alex Davidson appears to be getting his eye in with increasing grade and continuity through time.

Drill baby drill.

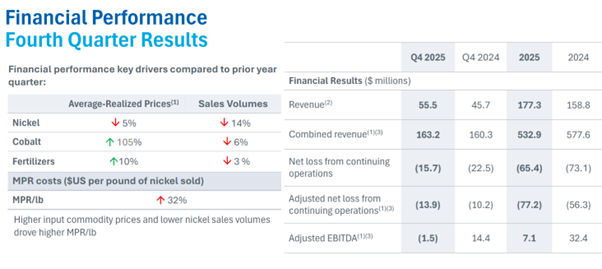

Sherritt: A wild-ass punt?

The last thing I did this week before boarding my flight to London was sign a subscription for an investment, or should I say a wild-ass-punt in Sherritt International (S:TSX) arguably the highest beta battery metal stock on the planet.

Sherritt is one of the worlds best known nickel producers having pioneered nickel extraction technology in its joint venture Moa Bay mines in Cuba in the 1950’s.

Sherritt owns 50% and the Cuban Government 50% of its Cuban nickel and cobalt mines then ships the valuable nickel and cobalt in a semi processed form to its Fort Saskatchewan nickel refinery in Alberta, Canada.

Not for Widows or Orphans

Sherritt is NOT for widows and orphans. Sherritt lost C$15.7 million in the December quarter of 2025 had cash of C$13 million at year end AND C$320 million of debt. That debt was recently trading around 60 cents in the dollar meaning investors thought Sherritt is likely to default on its debt obligations.

On March 30th Sherritt announced a non-brokered private placement of up to C$50 million at C$0.21 per share. The most interesting thing about the news release announcing the offering was this:

“As part of the Private Placement, Seymour Schulich, through a corporation controlled by him, has agreed to subscribe for up to 68,600,000 Common Shares for aggregate gross proceeds of up to $14,406,000.”

Schulich co-founded Franco-Nevada with Pierre Lassonde in 1982 — yes, the same Franco-Nevada mentioned above that owned the Ken Snyder mine and has been Canada’s best-performing mining company since inception.

Schulich and Lassonde are as well regarded as any management team in any industry in Canada.

While a C$14 million investment in Sherritt maybe loose change to billionaire Seymour Schulich, he is also an astute mining investor and noted Canadian philanthropist.

Perhaps Schulich has a positive view that the Canadian government will provide financial assistance to Sherritt to protect 800 Canadian jobs and to retain its valuable, 100% owned Fort Saskatchewan metals refinery and associated fertiliser operations for the Canadian market.

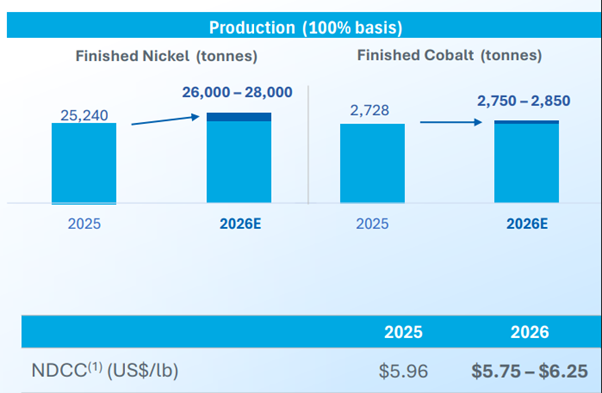

Leveraged Bet On Nickel

Sherritt is a financially leveraged bet on nickel which represents ~50% of revenue then fertiliser and cobalt.

Indonesia the worlds largest nickel exporter has signalled significant nickel production restrictions in 2026 which should have a positive effect on the nickel price.

Cuban Call Option

Sherritt’s second most important product is nitrate fertilisers prices for which are up sharply caused by the war in Iran. Sherritt’s input costs of Canadian gas and elemental sulphur in Cuba are more than offset by higher fertiliser prices in 2026.

If you believe in the possibility of Cuban regime change flowing from current US government sanctions on this small island 90 miles from the southern-most tip of the US mainland then Sherritt is a fabulous Cuba proxy.

The 1996 Helms-Burton Law prohibits US persons or companies investing in Cuba. If or when that law gets dismantled the effect of US capital flows into Cuba will be like standing under the Niagra Falls. Sherritt would be a significant recipient. Lets see what effect the fuel blockade and diplomacy of US Secretary of State and son of Cuban parents Marco Rubio has on Cuban politics.

Investors in Sherritt should view the ‘Cuban call option’ as unlikely but potentially explosive.

Catt Call 🐾

Hopefully your Easter egg hunt went well this Sunday.

We have described some old fashioned double digit yield Aussie coal investments: Yancoal, Whitehaven and Stanmore.

We have reviwed some important new high grade gold and silver exploration results from Hycroft Mining Corporation - our favourite precious metal bet.

And for the risk takers we have reviewed Sherritt International, arguably the worlds most leveraged bet on nickel with a Cuban call option.

Happy Egg Hunting!