Coffee with Catt: Issue #9 | Supercycle 2.0

AI: Critical Minerals and the Race for Global Supremacy

Welcome to the AI Supercycle

I worry that Artificial General Intelligence (AGI) will cannibalise my children’s future jobs.

Maybe it will take an AI accident involving autonomous weapons before nations agree to an AI Arms Treaty.

Yet I am optimistic that a higher intelligence could unleash the greatest productivity boom in human history.

What if the global AI capital expenditure cycle is only just getting started?

“AI represents a multi-year, structural capital formation wave of unprecedented scale.”

— Janus Henderson

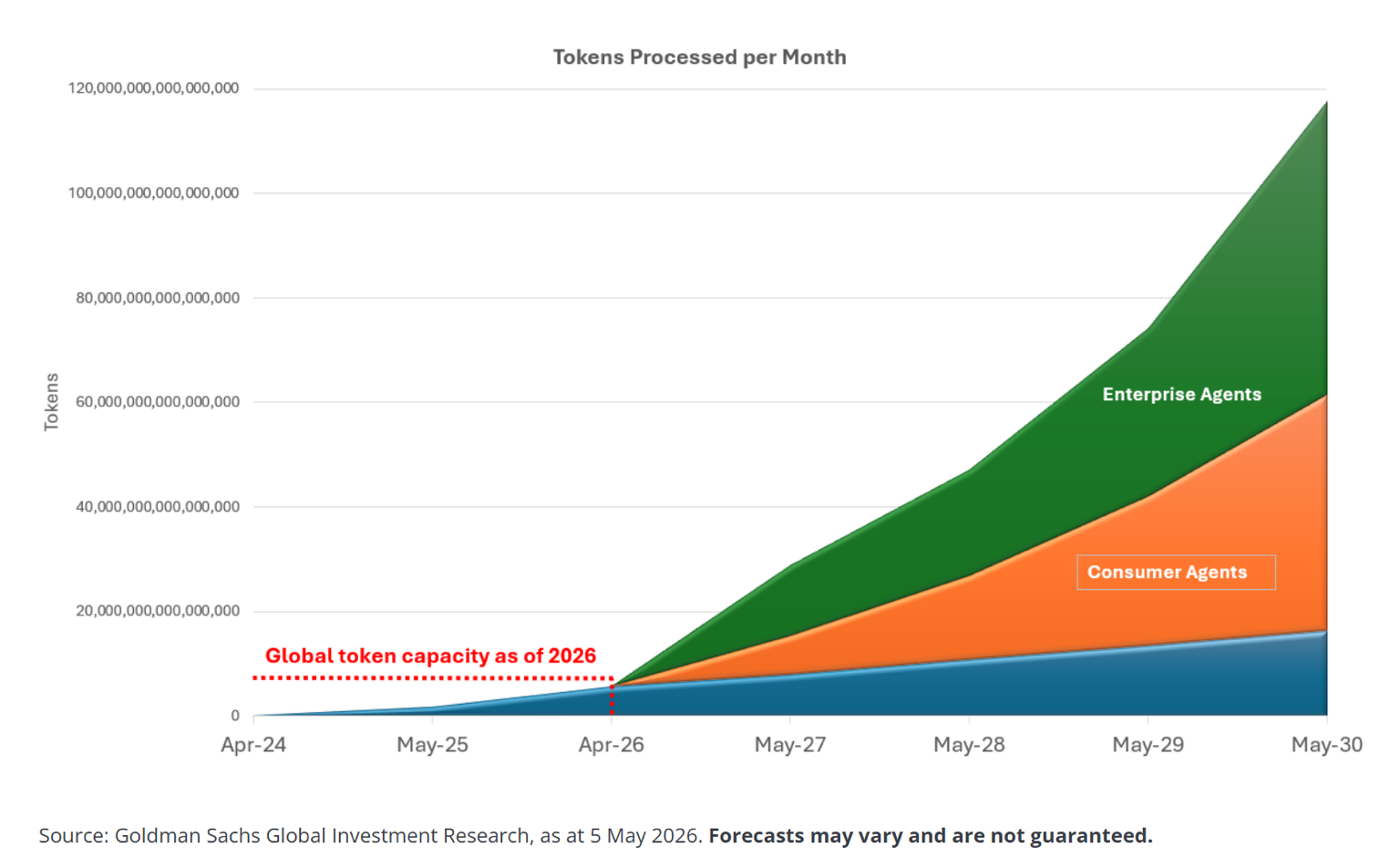

AI compute capacity is doubling every seven months.

Welcome to the AI Supercycle — or Supercycle 2.0.

What does this mean for commodity demand?

BlackRock’s Olivia Markham explained recently:

“Commodity demand is simply accelerating, and the commodity intensity of gross domestic product growth continues to rise.

The AI story is as much a power and metal story as it is a technology story.”

Most returns from mining equities are driven by a combination of rising commodity prices and rising equity markets.

How do the winners of Supercycle 1.0 help investors position for Supercycle 2.0?

Cuba, Critical Minerals and a Wild-Ass Punt

In the past two weeks I’ve visited three projects that should each produce metals critical for Supercycle 2.0, along with a multi-billion-dollar North American nickel and cobalt refinery that today trades for cents on the dollar.

Sherritt International’s future may be decided within weeks. It could be a bust or a ten-bagger.

I visited Sherritt’s 50%-owned Fort Saskatchewan nickel and cobalt refinery last month. The refinery can produce up to 38,000 tonnes per year of LME-grade nickel and cobalt.

Considering it was built in 1954, Fort Saskatchewan remains in remarkably good condition. The facility sits within Alberta’s Industrial Heartland, endowed with rail, water, energy, sulphur supply and demand for more than 200,000 tonnes per year of fertiliser from Canadian farmers.

The refinery’s nickel and cobalt feedstock comes from its joint venture mining operations with the Cuban government.

Recently, Sherritt has been taking evasive action to avoid US sanctions on Cuba, which were originally designed to displace the communist Castro regime.

Texan Republican billionaire and Trump campaign adviser Ray Washburne has made an offer that Sherritt may not be able to refuse.

As a result, Sherritt could soon become the only US government-approved Cuba investment proxy, with significant Cuban mining interests, a power station and receivables exceeding US$300 million from the Cuban government.

Background here:

“Sherritt — a Wild-Ass Punt”

Why This Supercycle Could Be Bigger Than China

Why is this commodity cycle potentially the most significant since China’s industrialisation in the 2000s?

Technology hardware, like all infrastructure, is built from materials and powered by energy.

Data centres, chip foundries, power stations and transmission infrastructure all require critical metals to store and move the digital tokens — or compute power — that are rapidly becoming the commodity of our age.

Data centres may become the intelligence factories that unleash global productivity, but they remain constrained by the energy and critical metals required to make them work.

What does the last commodity supercycle tell investors about where to position for this one?

From China’s Cities to AI’s Intelligence Factories

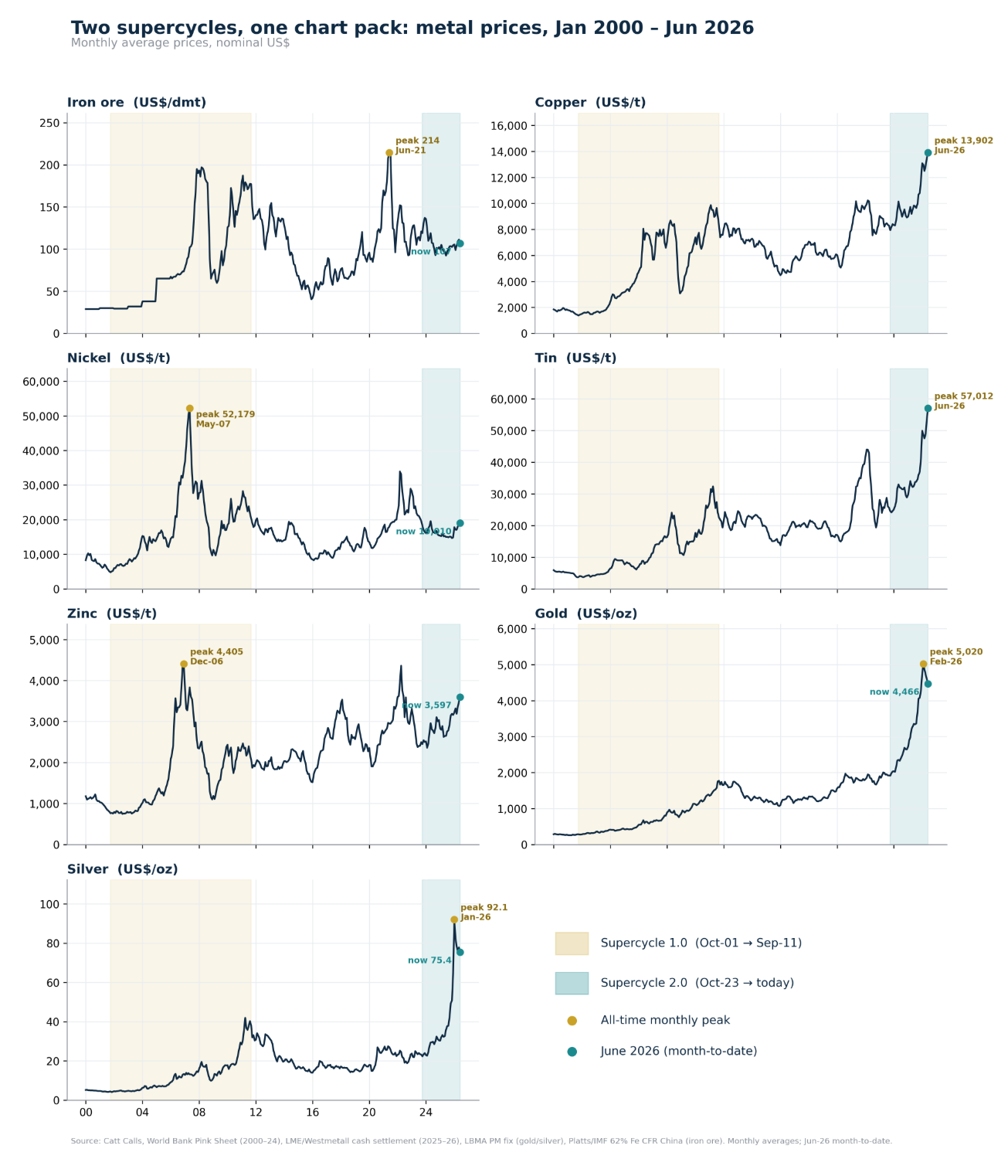

During Supercycle 1.0, iron ore and nickel led the way as China industrialised.

During Supercycle 2.0, the electrical metals — copper, silver and tin — are leading, while gold has resumed its historical role as the world’s premier monetary asset.

The China Supercycle 1.0

From cycle lows in the early 2000s through the peak in 2011, nickel, iron ore, copper and tin all rose roughly four to six times from their lows.

The urbanisation of China drove a doubling of iron ore production and a six-fold increase in iron ore prices between 2005 and 2010.

Nickel, driven by demand for stainless steel, experienced a seven-fold increase in price alongside a 250% increase in production volumes.

Australian and Brazilian iron ore supply doubled in response to those price incentives.

Copper prices, constrained by declining grades and ageing mines in Chile and Indonesia, are already more than one-third higher than in the previous cycle.

Gold has led commodities higher as it reclaims its status as the world’s premier monetary asset.

The Metals Powering Artificial Intelligence

This AI Supercycle favours metals that move and store energy.

Silver, lithium, cobalt, nickel and tin are all essential for batteries, electronic solder and capacitors.

Copper and aluminium are critical energy metals. Every major mining company wants a large, long-life copper asset in a stable jurisdiction.

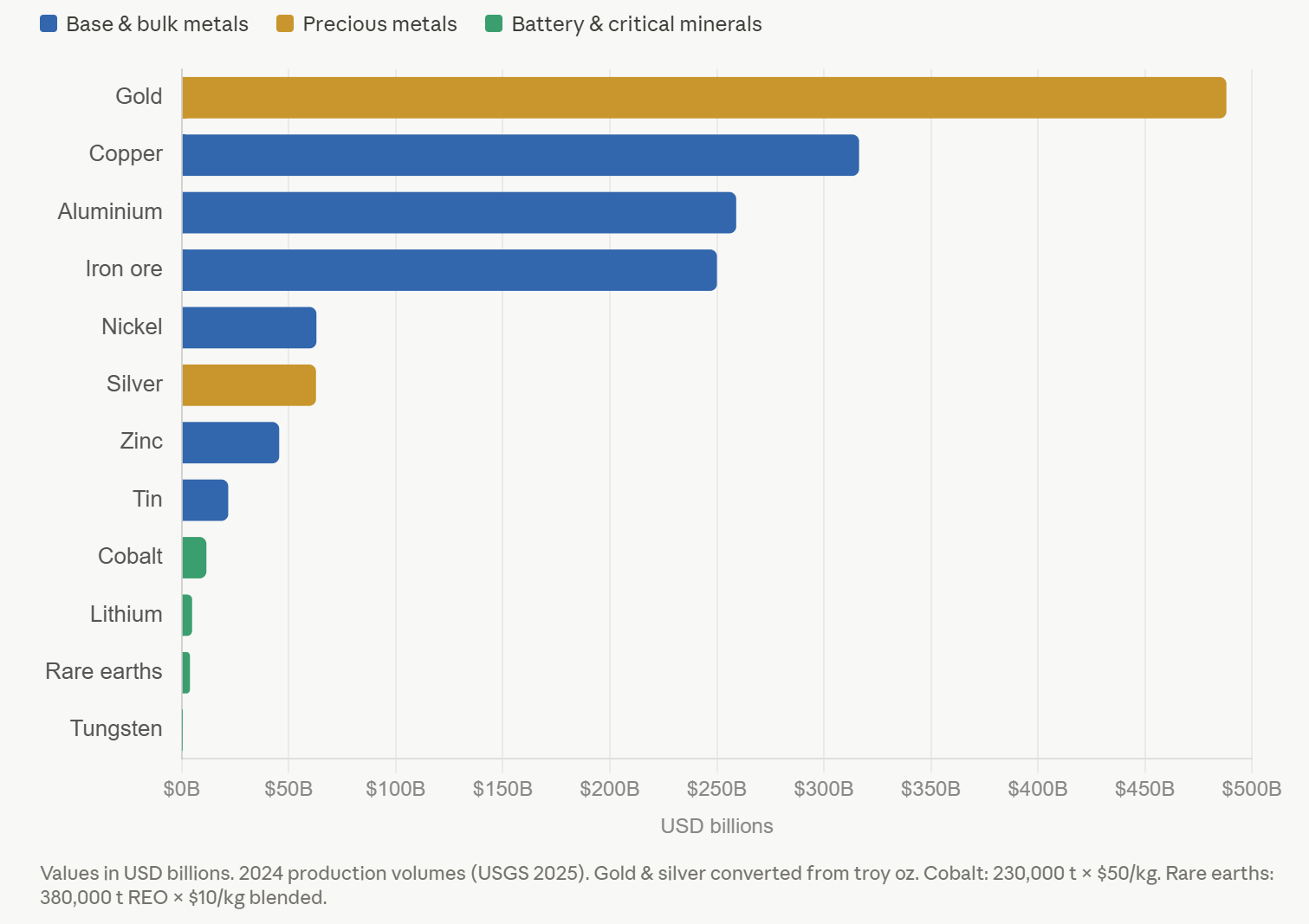

Value of 2024 production of important commodities at June 2026 prices:

China controls supply chains for rare earths used in magnets and tungsten used in military applications.

The risk for investors is that China increases supply to undermine competing foreign supply chains.

Lithium and aluminium, much like iron ore and nickel during the last cycle, are relatively abundant. Supply elasticity suggests prices are unlikely to remain elevated indefinitely.

Why Supply Constraints Matter More Than Demand

An important lesson from the 2000s supercycle was that durable commodity price appreciation requires constrained supply.

Goldman estimates that 60% of incremental copper demand through 2030 will come from electrical grid expansion.

Silver, the most electrically and thermally conductive element, is now in its sixth consecutive year of deficit. Solar panels and advanced electronics dominate industrial demand.

Silver is also money. Just ask a modern Indian bride whether she would prefer a silver dowry or a pile of rupees.

Silver is primarily produced as a by-product of gold, copper, zinc and tin mining, making supply relatively inelastic. Demand destruction will eventually emerge if prices rise too far.

Tin is the glue that holds every circuit board together. The denser AI hardware becomes, the more corrosion-resistant tin solder interconnections are required.

Nickel is essential for high-performance, energy-dense batteries. However, utility-scale storage increasingly favours cheaper lithium iron phosphate batteries.

Nickel supply is largely controlled by Indonesia — the OPEC of the nickel industry.

Four Critical Mineral Assets I Visited This Month

I believe there is no better way to understand the value of a project — and whether it can become a future mine — than to walk the dirt, lick the rocks and speak with the locals.

It’s not what people say, but how they say it, face-to-face, that still beats my favourite Claude AI toolbox.

Below is an introduction to four assets I visited during May. Watch Catt Calls for further updates.

First Tin — Taronga Tin Project

The Taronga Tin project owned by First Tin PLC (LSE:1SN GBP80 Million mkt cap):

First Tin’s Taronga project in the Australian state of New South Wales is four hours drive south of Brisbane. Taronga should be fully permitted, financed and under construction within a year. At current tin prices above US$50,000/ton Taronga should produce over US$100 million cashflow pa from 2029.

Tony Truelove the Tinman and First Tin Australian Operations Director at the Taronga Tin deposit, May 2026

Gippsland Critical Minerals — Fingerboards

The Fingerboards Rare Earth and Zircon project owned by unlisted Gippsland Critical Minerals (GCM) which is worth approximately A$75 million at recent funding valuations. GCM recently received ‘Major Project’ status from the Australian Federal Government who now have religion on ‘critical minerals’. Fingerboards should receive its key environmental permit from the Victorian regulator by the end of 2027.

Spirals being installed at Gippsland Critical Minerals test pit in May 2026

Gladiator Metals — Whitehorse Copper Project

The Whitehorse Copper Project owned by TSX listed Gladiator Metals (GLAD:TSX) was previously mined for copper and gold by Hudbay Minerals (HBM:TSX) in the 1980’s.

Well known City of Whitehorse residents the Coyne Family own 12% of Gladiator and are citizens of the Kwanlin Dun First Nation (KDFN) group. The Whitehorse copper project sits within the KDFN traditional lands.

Gladiator will likely outline an open pit resource of over 100 million tons of high grade, open pittable copper, gold, silver and molybdenum from its Cowley Park and Cub orebodies in 2027 with 50km of additional exploration upside. Gladiator's recent exploration success has followed a breakthrough in understanding that coincident gravity and electrical conductivity anomalies indicate where to find mineralisation.

Gladiator technical advisor Colin Jones and Yours Truly on site at Gladiator’s Whitehorse copper project, May 2026.

Sherritt International — Fort Saskatchewan Refinery

The Fort Saskatchewan Nickel and Cobalt refinery is 50% owned by TSX listed Sherritt International (S:TSX). This nickel and cobalt refinery with by-product 100% Sherritt owned fertiliser production would cost billions of dollars to construct today and has produced over three billion pounds of nickel Fort Saskatchewan - Refinery Process

The nickel and cobalt feedstock for Fort Saskatchewan comes from the Moa Bay Joint Venture with the Cuban government.

Sherritt announced on May 20th that the US State Department had approved the potential sale of 55% and control of Sherritt to Gillon Capital, a Dallas based family office. Gillon is led by Ray Washburne a prominent fundraiser and advisor to President Trump who ran the Overseas Private Investment Corporation (OPIC) from 2017-2019 which has since become the US Development Finance Corporation or DFC.

Supercycle 2.0: Halfway There or Just Beginning?

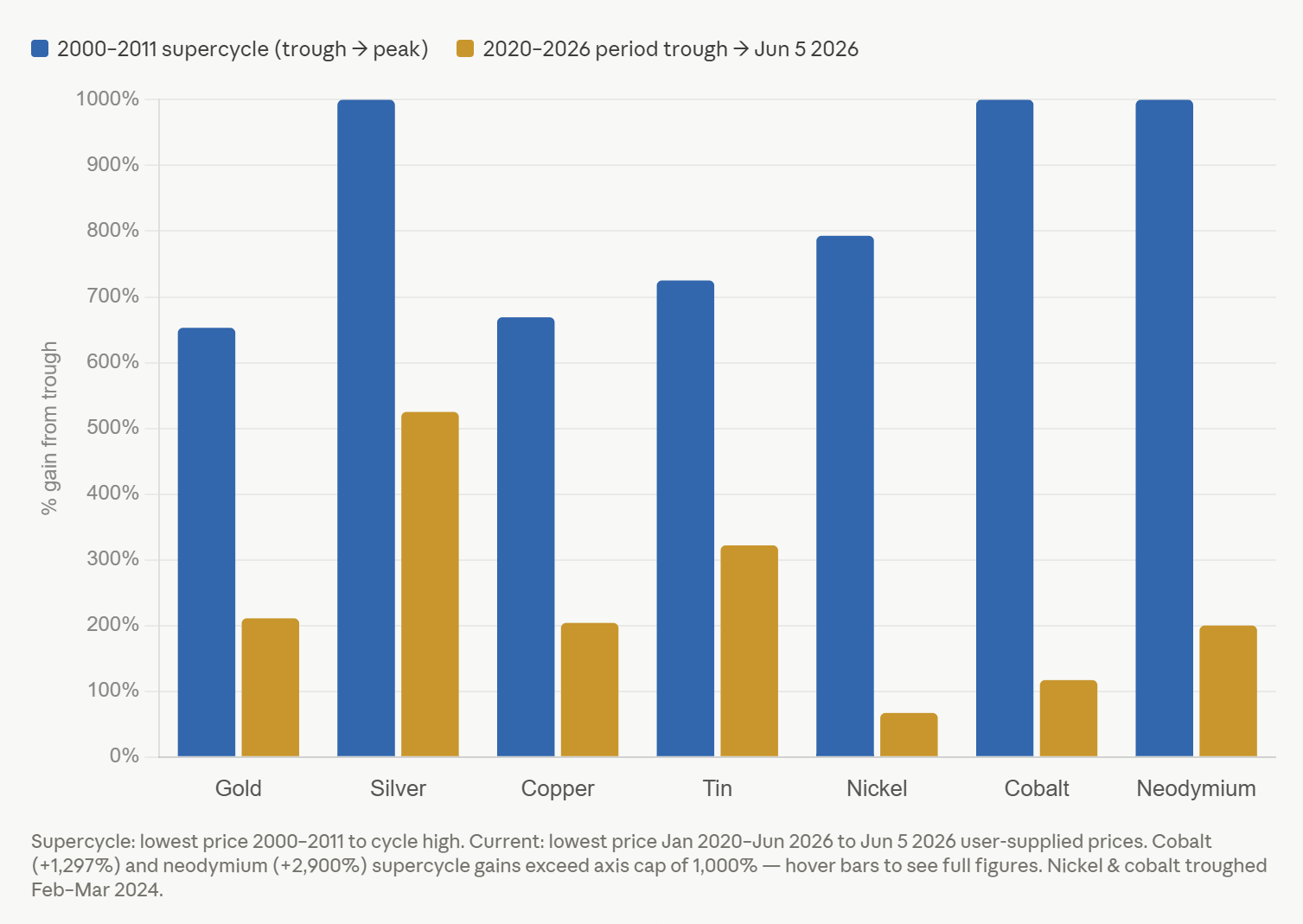

Measured by percentage gain from trough lows to cycle highs this Supercycle 2.0 is half over for silver and tin and barely started for nickel, cobalt and neodymium. Copper and gold have appreciated about one third as much this cycle as they did in the last.

Catt Call: The Commodity Supercycle 2.0 has just begun.

New investors worry that current commodity prices will fall making miners look expensive.

A comparison with the last Supercycle shows that the opposite is true, prices of the leading metals this cycle are at most half way through their price move.

The race for AI supremacy is existential and it has just begun. Critical minerals and energy will empower the world's next Superpower and its mastery of Artificial Intelligence

The Commodity Supercycle 2.0 has just begun